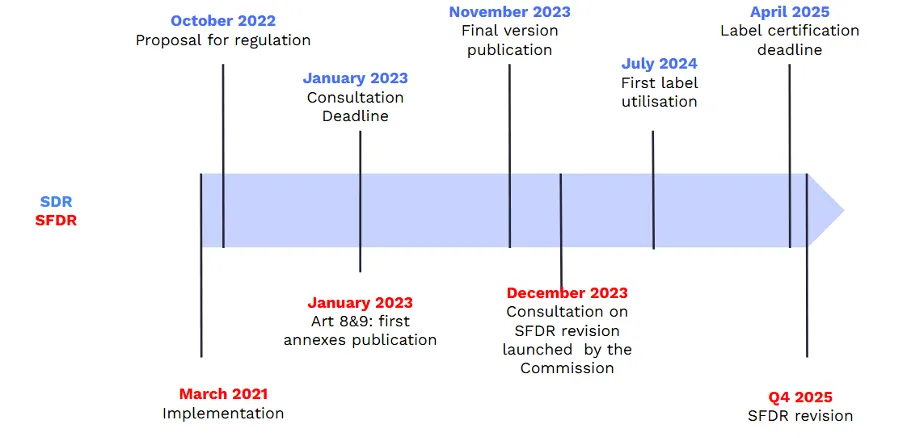

April has been a month rich in developments for sustainable finance in Europe, beginning with the key date of 2nd April, which marked the entry into force of SDR (Sustainable Disclosure Regulation) in the United Kingdom.

Indeed, the SDR regulation, designed to improve transparency of financial products labelled as "sustainable", represents a significant milestone in the construction of a post-Brexit non-financial framework, distinct from yet parallel to the European Union's SFDR (Sustainable Finance Disclosure Regulation).

The implementation of this new regulation across the Channel comes at the very moment when the European Commission is undertaking an in-depth overhaul of SFDR, following several months of consultations and critical feedback from the financial community. Thus, SDR and SFDR appear to mirror each other, offering Europe two visions of sustainable finance for a single common goal: to provide a transparency regime and clarify what constitutes a sustainable product. It is therefore interesting to examine the connections between these regulations, their similarities as well as their differences.

The SFDR regulation came into force in the European Union in 2021 to harmonise and strengthen sustainability in the financial sector. It requires various stakeholders to be more transparent about the environmental and social responsibility of their investments, with varying levels of requirements depending on whether their products fall under Article 6, 8 or 9. By the end of 2024, the combined assets of Article 8 and 9 funds represented 60% of the entire EU fund market according to Morningstar, although Article 6 funds still attracted the most inflows.

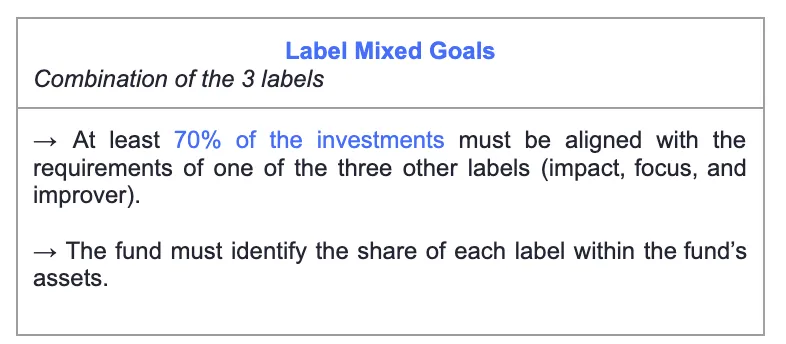

SDR is the British response to the need for sustainable finance regulation. The framework aims to be readable and demanding for investors and is based on a simple, non-hierarchical classification of products: Sustainability Focus, Sustainability Improvers, Sustainable Impact and Sustainability Mixed Goals.

SDR was conceived as a comprehensive package combining both an anti-greenwashing rule and requirements for naming and marketing for asset managers. By the end of the first quarter of 2025, 80 funds opted for one of the 4 labels and 325 others provided their first consumer-oriented disclosures. As Mark Spooner, Sustainable Investing Associate at Fidelity, points out, "SFDR and SDR share a common philosophy but have different orientations: whilst SFDR is intended as a disclosure regime, SDR is a regime focused on labels".

To understand the regulatory dynamics in sustainable finance, the timeline below puts into perspective the key milestones of SFDR and SDR, two frameworks whose evolution reveals certain complementarities on both sides of the Channel:

Whilst the SFDR Regulation applies to all financial market participants operating in the European Union or marketing financial products to European investors, SDR currently applies only to financial actors in the United Kingdom.

Moreover, although different, the classifications put forward by SFDR and SDR seem to demonstrate certain similarities. While an SFDR Article 6 fund does not meet any requirements to obtain an SDR label, SFDR Articles 8 and 9 have multiple commonalities with SDR labels. Although SDR labels are not hierarchical, in practice we observe that Article 8 or 9 funds have been able to obtain SDR labels. In its Policy Statement (page 122), the FCA offers a comparison of qualification criteria and relevant SFDR information that companies can use to satisfy SDR requirements, which reinforces this analogy.

The Green Future fund, for instance, from the English asset management company EdenTree, has just been labelled "Sustainable Impact". Under SFDR, the fund is also Article 9! On its website, publications specific to both regulations are present, allowing us to observe a certain consistency in the sustainability objectives and quantitative thresholds displayed.

SDR side: The sustainability objective defined by the fund for its "Impact" label is to support a reduction in greenhouse gas emissions through investments in companies whose products and services provide solutions to climate change, and the fund commits to having at least 70% of its assets aligned with this objective.

SFDR side: The annexes mention a minimum sustainable investment of 80% with an environmental objective.

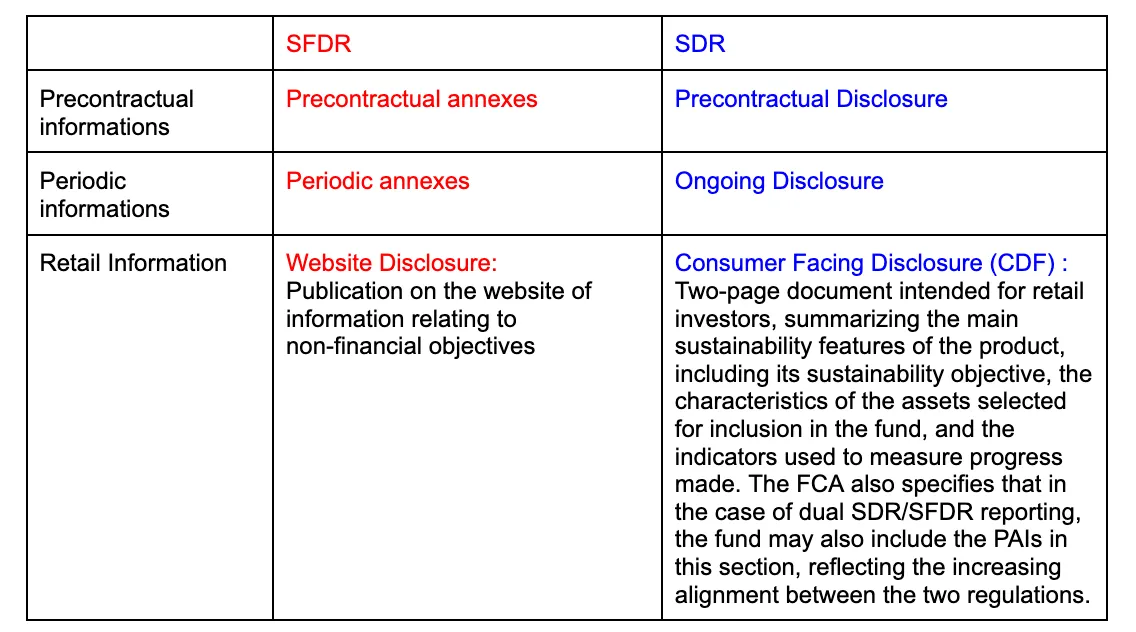

When a British fund uses an ESG label or terminology, it is required to incorporate sustainability information in documents intended for investors (Consumer Facing Disclosure), as well as in its precontractual annexes and ongoing annexes. These must be added to the fund's prospectus and annual report respectively. According to Mark Spooner, these various documents, particularly the CFD, demonstrate that SDR places particular emphasis on consumer protection, aiming to guarantee them concrete sustainability outcomes.

❌ This absence of precise requirements stems from the wishes of British financial institutions who expressed their views during the FCA consultation.

Despite regulatory divergences, some asset management companies do not hesitate to rely on documents published under another legal framework to enhance the information provided to investors. For example, the English wealth management company Saint James Place published its SFDR website disclosure on its site, then adapted it to also meet the requirements of the SDR regulation. This continuity shows that SFDR requirements have influenced the SDR framework.

As specified by the FCA in its Policy Statement, the consultation that took place in January 2023 to draft an initial outline of the SDR regulation aimed to adopt a classification system similar to the SFDR regulation. Now, British investment funds define their sustainability ambition and choose the label that best suits them. The name of the label provides a first indication of the investment strategy adopted, filling a gap in Articles 8 and 9, which do not currently allow for a clear understanding of the intention underlying each investment strategy.

In parallel, SFDR faces numerous criticisms, a phenomenon accentuated by the publication of the British model. In December 2023, just one month after the final publication of the SDR regulation incorporating this voluntary labelling system, the European Commission launched a public consultation to invite key stakeholders to express their views on SFDR and propose modifications. The goal was to identify potential gaps by focusing on "the ease of use of the regulation and its ability to play a role in combating greenwashing". According to Mark Spooner, SDR seeks to avoid SFDR's pitfalls by requiring ESG funds to specify more clearly what they actually accomplish.

For its part, the FCA continues to place great importance on the regulatory advances of SFDR and supports greater alignment between the two regulations.

The French Financial Markets Authority (AMF), the ESAs and the Platform on Sustainable Finance have made public their response to the European Commission consultation mentioned above by proposing a categorisation system aimed at replacing the current use of Articles 6, 8 and 9. Given that the Platform on Sustainable Finance is mandated by the European Commission, we will focus here on its recommendations which propose the creation of 3 new categories of sustainable funds: Sustainable, Transition, and ESG Collection.

Just like adopting an SDR label, belonging to a category with SFDR 2.0 would require compliance with specific criteria accompanied by specific reporting standards. Thus, compliance with a single category would simplify the information to be transmitted to investors, who could be reassured by such a system. It should be noted that the Platform on Sustainable Finance reminds us that these categories are not labels, as they do not have the same structure or verification system.

This label can apply to funds that focus on opportunities created by the transition to sustainable and carbon-free economies. This dynamic can be observed, for example, in the strategy of the FP WHEB Sustainability Impact Fund, which invests in companies in the health, safety, resource and waste management sectors. Like its first version, SFDR 2.0 does not provide for a dedicated impact category.

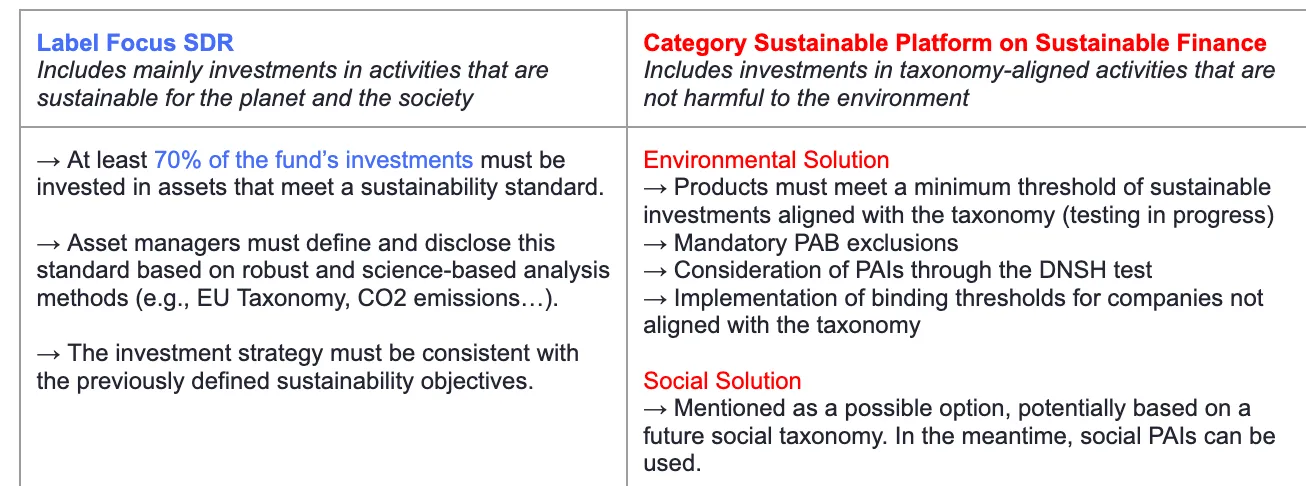

According to SDR, this strategy concerns investments in assets deemed "sustainable", whether in regard to the European Taxonomy or according to other frameworks established by British funds. The Focus label thus appears as the British equivalent of the "Sustainable" category defined by the Platform on Sustainable Finance. It should be noted that SDR labels do not explicitly distinguish between environmental and social aspects, unlike the category introduced by SFDR 2.0, which integrates for the first time the notion of social solution, based on social PAIs or even a potential social taxonomy.

The introduction of a transition category by both SDR and SFDR 2.0 highlights efforts to move towards a more sustainable economy through investment in activities that are not yet green but far from brown. This is the SFDR 2.0 category and SDR label where the most similarities can be observed. The requirement to display targets and important milestones echoes the transition plans of the ESRS or the establishment of decarbonisation trajectories.

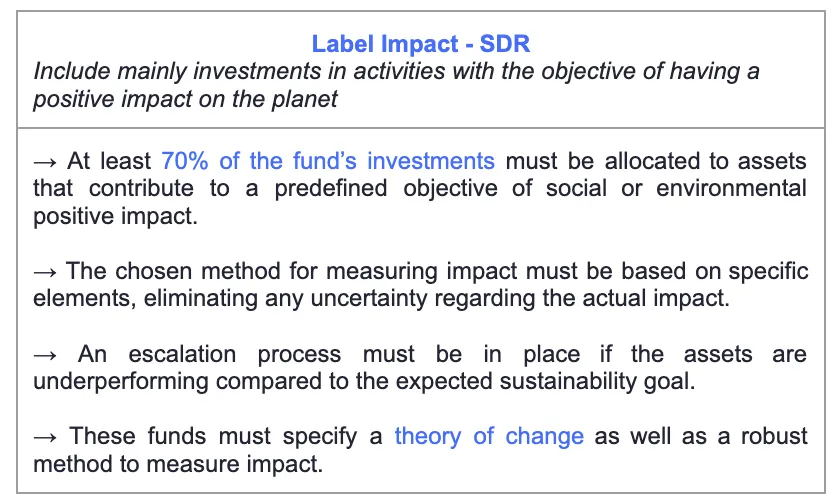

Primarily includes investments in activities that have the explicit objective of delivering a positive impact on the planet.

→ At least 70% of the fund's investments must be invested in assets that contribute to a predefined objective of positive impact on the environment or society.

→ The chosen impact measurement method must be based on specific elements, making any uncertainty regarding the actual impact impossible.

→ An escalation process must be implemented if assets are not performing sufficiently against the sustainability objective.

→ These funds must specify a theory of change as well as a robust method to measure impact reliably.

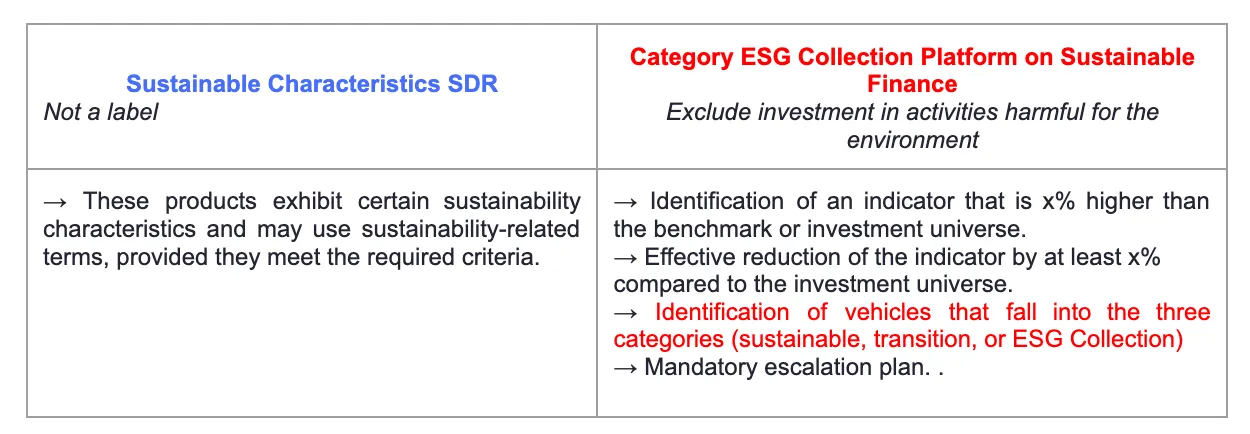

The "ESG collection" category from the Platform on Sustainable Finance is a first step towards sustainable investments through mandatory exclusions of environmentally harmful activities. With its more moderate ambition, it is possible to compare this category to SDR's "Sustainable Characteristics". Even though the latter is not a label, funds can decide to comply with more flexible requirements in order to begin integrating ESG considerations. It should be noted that funds in the "ESG Collection" category are subject to the obligation to determine which assets are considered "sustainable", "in transition" or simply present "environmental characteristics", a principle strongly reminiscent of the "SDR Mixed Goals" label, which aims to provide a framework for financial products that follow one or more of the investment strategies mentioned above.

The comparison of regulatory requirements between the European Union and the United Kingdom highlights British influence in the revision of SFDR. Thus, the evolution of one regulation seems to influence the other. Mark Spooner also agrees with this view: according to him, for cross-border fund managers, interoperability between regulations is well received and deemed relevant. During her hearing before the European Parliament on 6th November 2024, the designated Commissioner for Financial Services, Maria Luís Albuquerque, expressed her desire to evolve SFDR towards a product categorisation system inspired by the British model. Such an evolution would better frame ESG practices, limit greenwashing and give a central place to transition approaches, an essential lever for achieving a green economy. This revision would provide a precise framework for numerous companies representing "the majority of our productive sector". The hypothesis that SFDR and SDR might be a "match" is therefore becoming clearer... Answer in the last quarter of this year.

.webp)

.webp)